Budgeting.

It's not a dirty word, I promise. For most of the past year I've been tracking all of my spending, and adding it to a spreadsheet on a month-by-month basis. A few small cash expenditures almost certainly slipped through the cracks, but overall my spreadsheet represents everything that comes both in and out.

Before I started tracking, I naïvely assigned fairly arbitrary 'budgeted' values to the various categories I'd made up off the top of my head. The reality of my spending adjusted those numbers quite a bit. I'd like to share a little bit of my financial tracking system here, as well as illustrating the lessons I've learned.

The Equation

I've always loved being able to reduce a seemingly complicated system into its simpler parts. If all the rest can be derived from a few core principles, why bother remembering all the fiddly details? Despite all the specific, complex, and/or baffling budgeting tips out there, it all comes down to one fundamental equation.

$ in > $ out (1)

As long as this holds, your financial plan is sound. It's really all you need. All the rest (earn more, use x or y pesky little money-saving tip, clip coupons, etc.) follows.

The Tools

For day-to-day tracking, I'm in love with the pocketmod. It's really just a way of folding a piece of paper into a little book, and you can specify the type of list or information you want on each page, and it will let you print it out. I use the first two pages for a running to-do list, and the rest for recording transactions. It's super low-tech, but it works for me, and always lives in my bag.

I know people out there love Mint, Quicken, etc., but I'm a fan of old-fashioned spreadsheets. More specifically, I love Google Docs simply because I can update and read my budget from anywhere, and never worry about not having an up-to-date version of the file.

To calculate how long it will take to pay off various debts, I was thrilled to find this debt snowball spreadsheet. It lets you choose from a variety of methods, including the downright sobering figures on how much interest you'll be paying for how long if you choose to only make minimum payments. While the higher-interest-first method makes the soundest financial sense in that you wind up paying less interest, there's a lot to be said for the psychological encouragement that comes from the lowest-balance-first plan since you get more victories earlier in the game. Fortunately, for me those wound up being one and the same. Thanks to this sheet I know exactly how much to throw at each debt in turn, and exactly how long it will take. You can also enter in 'snowflakes,' or one time payments, in case you want to toss a little extra money on the highest priority debt, and it will take that into account. Get Rich Slowly also posted a review of this spreadsheet.

Lessons Learned

- Don't bother setting initial budget values. Just track your actual spending, and go from there.

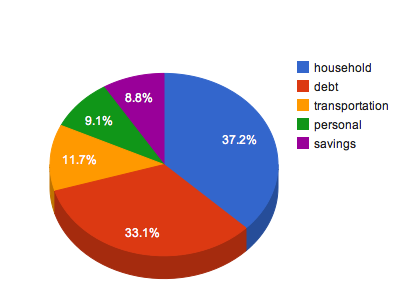

- Feel free to revise your categories. Today I wen through and made a brand new sheet for this year's tracking, and took the opportunity to reformat, recategorize, and edit. There were several categories that are no longer relevant, and instead of having a random list I have to poke through every time I want to add a value, I sorted them into categories. The pie chart at the top of this post has my new projected monthly expenditure breakdown for 2012. There's not a lot in the 'savings' wedge, admittedly, but that's because I'm throwing everything I can at my debt snowball right now.

- If you're using a spreadsheet for tracking spending, I highly recommend a second column next to each month's numbers, for notes. That way, in case you wonder why the heck your 'other' category was so high in April of last year, you'll know that it was because your best friend got married and you suddenly had to buy an overpriced chartreuse layer cake gown. If you set the column to not wrap the text, then you can simply make it super narrow and it effectively disappears. Then it won't be in the way of looking at the overall figures and you can always expand it if you get curious.

- Tracking really isn't that hard! I got lazy sometimes and would figure that I could always just look at my debit card bill and figure it out from there. Unfortunately, the 'what the heck was this charge for' line on account statements are often far from clear, and I've spent my share of time looking up addresses in an effort to divine where I spent that particular $15. Just writing it down when I'm at the store is a lot easier.

- Put a place for income on your spreadsheet. The corollary to this is that you get a savings entry, being the difference between your income and your spending. This number gives you a healthy little panic attack when it goes negative, meaning that you broke the cardinal rule. See equation 1!

- Don't accrue more debt while you're paying it off. My general financial awareness improved by several orders of magnitude when I set a personal moratorium on credit card spending. When you're spending real money instead of pretend numbers on a statement, you suddenly care a lot more. A couple of times I've gotten pretty close to being genuinely broke, and then had to become a serious cheapskate for a week or so until my next paycheck came in. It was a good experience. While I was previously in a pretty good habit of paying off what I spent on the credit card (above a certain amount of permanent balance; bad me!), it just feels different when you feel each purchase rather than just tossing whatever lump sum you've got around on the card later. I'm definitely spending less on trivial things this way.

Some Final Thoughts

Tracking my spending and building a real budget has been quite an illuminating process, and is actually kind of fun. You don't need to learn complicated software or get a budgeting app, and the manual process is probably more satisfying anyway. Give it a try!

No comments:

Post a Comment