My blogging goal for January was to update at least 8 times. Looking back, it appears I managed a total of 4 posts.

Some might call that abject failure; I call it partial success. I did accomplish the more fundamental goal of paying more attention to this thing and updating more often than I had been. Stay tuned for February's challenge!

1.31.2012

1.23.2012

progression

In the continuing financial theme that seems to have manifested this month, today I completed a milestone!

If step 0 of Operation: Debt Freedom was to curb all credit-based spending, the subsequent steps then must involve paying off the balances on each extant line of debt. As of this morning, my highest-interest credit card finally has a zero balance. Count step 1 completed!

Since I'm using the debt snowball method, this means that my snowball just grew a little bigger and picked up some speed. I no longer have any payments to make on this card, so all the allocated money for debt reduction (aside from required minimum payments) can now all be piled on my next-highest-interest debt. In my case this means my other credit card, which will unfortunately take a fair while to pay off due to quite a few travel-related expenses that have been sitting on there and building up interest.

Hooray for small triumphs!

1.10.2012

a financial retrospective

Today I played around a little with my records of my 2011 spending. Above is a pie chart of where my money went, on average, each month. What are the categories? Let's take a closer look. They're in a fairly random order, since my spreadsheet for 2011 was not all that well organized. Rest assured that the 2012 one makes a bit more sense as a result of my experiment so far.

|

| 2011 average monthly spending ratios |

Overall, I'm pretty okay with this. The majority of my spending was apparently focused on paying off debt, which I'm a fan of. However, during this time I was still putting more charges on the credit card(s), so some of that is masking other spending. It's a slightly convoluted system, and I'll definitely be keeping closer tabs in the future.

The second biggest category was food. Not eating out, but groceries. See previous post; we're working on this.

I did not track wedding expenditures in this form, because

- it would have thrown off all the numbers by quite a bit, and

- it was a one-time cost, and I didn't want to be stressing about it too much.

We had a relatively inexpensive wedding, and it helped my sanity to not be tracking every penny and having to look at that rather large entry. Maybe that was a wrong call, but it's what I did. Consequently, I gave up entirely on tracking during the month of October for during the wedding and honeymoon, so there's a gap in the data. That said, the averages still hold; there's just a dropped month in there.

Of the money I spent, the above bar chart says where it went. But how much of my income actually got spent? For that, I need another section of my spreadsheet. While looking at expenditure ratios wasn't particularly depressing, this was. I figured out what proportion of my income was not spent each month, and plotted that. I'll let the chart tell its own story:

|

| monthly savings as proportion of income, 2011 |

The grand average proportion of income that was not spent in one way or another (rounded to two significant figures): 0.012, or 1.2%. Yikes.

Apparently I particularly fell off the bandwagon in July. What happened in July?

- I got an oil change, which is somewhat expensive since I use full synthetic oil.

- I bought a digital camera for myself and Mr. Geek, just because we didn't have one.

- I spent nearly $300 on groceries just out of my account, and probably more than that from the shared account. We took a trip out of town for Mr. Geek's final fitting for his wedding ensemble, which perhaps ought to be tagged as a wedding expense and removed from the tally, but we took a mini-holiday while we were there so it remained a 'vacation' expense.

- I spent a ridiculous amount on audiobooks that month, since I was still driving my very long commute by myself at that time and needed them to keep awake.

- Finally, I bought a significantly overpriced (but fabulous!) retro swimsuit for a 4th of July pool party, except that it didn't arrive in time anyway.

Ouch! On the plus side, I apparently totally rocked in September. However, it's also possible that I simply failed to record some of my expenses. There are still some bugs in the system.

It's really eye-opening to have all these numbers to play with, and to be able to see trends over time. Hooray for spreadsheets!

1.04.2012

eat food

I found the above fabulous flowchart from The Summer Tomato today. It puts me in mind of Michael Pollan's summary of the entirety of his own advice, 'eat food, not to much, mostly plants.' How many of us truly follow this type of advice? Unless I've bought the given product before, I'm constantly reading labels and getting jumpy if there are unpronounceable ingredients or my favorite, 'natural flavoring.' However, I'm sure I still purchase and eat more than my share of not-food.

In my budgeting adventures yesterday, Mr. Geek and I sat down to take a real hard look at our financial situation. Our main expenditures are for housing, fuel, and food. Housing costs are pretty stable and unchangeable, since our rent isn't likely to change and we already keep the house between 55 and 65 F during the winter. It was the spreadsheet cell labeled 'grocery' that was truly staggering. There's absolutely no reason, even with rising food prices and an unstable economy, that two people should need to spend that kind of number just to keep fed.

For reference, I've been tracking my own spending for nearly the past year (see immediately previous post), but have not been following the spending out of our joint account. This despite the fact that I have personally used the shared debit card for an awful lot of grocery shopping, for the simple reason that I didn't have enough money in my own account at the time. Bad me for not paying more attention!

In addition, while I do make an effort to take frugal measures when shopping (scouring the circulars to figure out where to do the week's shopping, clipping coupons when they present themselves, stocking up on stuff when it's on sale, etc.), obviously there's been more than a little mindless spending when it comes to the grocery store. We do tend to splurge on good ingredients fairly often, since we both love to cook and are amateur foodies. Food spending falls into three basic categories:

- Deliveries from our local CSA: I'm not giving this up unless I absolutely have to. Fresh, in-season, local food is absolutely worth it. I need my fresh veg. Maybe it should drop to every other week.

- Pet food: our dog and cat are both on species-appropriate whole prey model raw diets, but I already buy their meat only when on sale and portion and freeze it myself, so I seriously doubt this eats up too much of the budget. The guinea pigs get fresh veggies along with their pellets and hay, but it's generally leftover bits from prepping ingredients like carrot peels, stuff that's about to be past its prime anyway, or cheap bins of leafies from Costco.

- General grocery

So what really is to blame?

- Too much processed food: this is pretty minor, since we do both cook so much. But why are we always buying so much store bread when I love baking? The answer, of course, is that I'm just a little too lazy and don't have enough of a plan to make the time to bake enough bread for the week. This applies to multiple things; what business do I have ever buying pickles, when I've canned up so many jars?

- Over-purchasing: looking into our pantry is a fear-inspiring endeavor, since it seems the piles of goods may fall on you at any moment. Heaven help you if you wanted to add something to a shelf. The fridge, similarly, is quite a deathtrap.

- Lack of inventory management: last year sometime we organized and inventoried everything in the pantry, fridge, freezer, and chest freezer. However, it hasn't been updated particularly regularly, and so has fallen into irrelevancy. Not knowing what we already have leads to both over-purchasing, and...

- Food waste: throwing away what was perfectly good food and only isn't due to inattention is idiotic. Far too many containers of leftovers get lost at the back of the fridge only to be discovered when they're developing intelligent life, and far too much good produce goes to the crisper drawer only to turn to slime out of either negligence or simply not thinking of something to do with it.

The solution: in addition to re-instituting some sort of inventory management system, I think it's finally time to try out menu planning. Ordinarily meals are crafted by staring into the fridge for a while until an idea occurs to one of us. This means that we both have to keep a huge assortment of ingredients on hand at any one time for any unknown genres of food (hence part of the overstuffed fridge problem) and that shopping is done on the simple method of replenishing whatever gets used up whether it's truly a staple or not, coupled with whim. And whim gets expensive. My CSA orders are similarly random, and I just guess what we might find a use for in the coming week, thus leading to languishing slimy lettuce. There must be a better algorithm to find a practical optimum for the system.

In theory, sitting down to plan a week's menu shouldn't take too much time, and should allow for both more selective shopping and less stress after work. I've never done this sort of thing before, aside from planning a few days' worth of bento lunches at a time. We'll see how it goes.

Along with all those plans, we're talking about a new policy that prohibits using the shared account for food. If I have to use my own money, it's quite likely that the pressure will be a great help in enforcing frugality. It's working for everything else, so why not apply it to this as well?

Along with all those plans, we're talking about a new policy that prohibits using the shared account for food. If I have to use my own money, it's quite likely that the pressure will be a great help in enforcing frugality. It's working for everything else, so why not apply it to this as well?

I think there may be all of three people who know this blog exists at this point, but in case anyone has input, what do you think? Any thoughts or tips on menu planning or reducing grocery expenditures? How are these things handled at your house?

1.03.2012

conservation of dollars

Budgeting.

It's not a dirty word, I promise. For most of the past year I've been tracking all of my spending, and adding it to a spreadsheet on a month-by-month basis. A few small cash expenditures almost certainly slipped through the cracks, but overall my spreadsheet represents everything that comes both in and out.

Before I started tracking, I naïvely assigned fairly arbitrary 'budgeted' values to the various categories I'd made up off the top of my head. The reality of my spending adjusted those numbers quite a bit. I'd like to share a little bit of my financial tracking system here, as well as illustrating the lessons I've learned.

The Equation

I've always loved being able to reduce a seemingly complicated system into its simpler parts. If all the rest can be derived from a few core principles, why bother remembering all the fiddly details? Despite all the specific, complex, and/or baffling budgeting tips out there, it all comes down to one fundamental equation.

$ in > $ out (1)

As long as this holds, your financial plan is sound. It's really all you need. All the rest (earn more, use x or y pesky little money-saving tip, clip coupons, etc.) follows.

The Tools

For day-to-day tracking, I'm in love with the pocketmod. It's really just a way of folding a piece of paper into a little book, and you can specify the type of list or information you want on each page, and it will let you print it out. I use the first two pages for a running to-do list, and the rest for recording transactions. It's super low-tech, but it works for me, and always lives in my bag.

I know people out there love Mint, Quicken, etc., but I'm a fan of old-fashioned spreadsheets. More specifically, I love Google Docs simply because I can update and read my budget from anywhere, and never worry about not having an up-to-date version of the file.

To calculate how long it will take to pay off various debts, I was thrilled to find this debt snowball spreadsheet. It lets you choose from a variety of methods, including the downright sobering figures on how much interest you'll be paying for how long if you choose to only make minimum payments. While the higher-interest-first method makes the soundest financial sense in that you wind up paying less interest, there's a lot to be said for the psychological encouragement that comes from the lowest-balance-first plan since you get more victories earlier in the game. Fortunately, for me those wound up being one and the same. Thanks to this sheet I know exactly how much to throw at each debt in turn, and exactly how long it will take. You can also enter in 'snowflakes,' or one time payments, in case you want to toss a little extra money on the highest priority debt, and it will take that into account. Get Rich Slowly also posted a review of this spreadsheet.

Lessons Learned

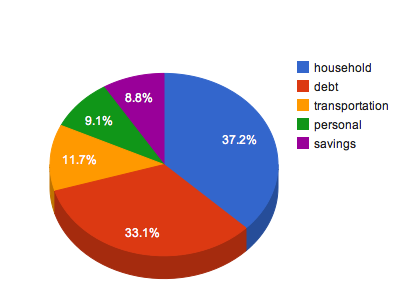

- Don't bother setting initial budget values. Just track your actual spending, and go from there.

- Feel free to revise your categories. Today I wen through and made a brand new sheet for this year's tracking, and took the opportunity to reformat, recategorize, and edit. There were several categories that are no longer relevant, and instead of having a random list I have to poke through every time I want to add a value, I sorted them into categories. The pie chart at the top of this post has my new projected monthly expenditure breakdown for 2012. There's not a lot in the 'savings' wedge, admittedly, but that's because I'm throwing everything I can at my debt snowball right now.

- If you're using a spreadsheet for tracking spending, I highly recommend a second column next to each month's numbers, for notes. That way, in case you wonder why the heck your 'other' category was so high in April of last year, you'll know that it was because your best friend got married and you suddenly had to buy an overpriced chartreuse layer cake gown. If you set the column to not wrap the text, then you can simply make it super narrow and it effectively disappears. Then it won't be in the way of looking at the overall figures and you can always expand it if you get curious.

- Tracking really isn't that hard! I got lazy sometimes and would figure that I could always just look at my debit card bill and figure it out from there. Unfortunately, the 'what the heck was this charge for' line on account statements are often far from clear, and I've spent my share of time looking up addresses in an effort to divine where I spent that particular $15. Just writing it down when I'm at the store is a lot easier.

- Put a place for income on your spreadsheet. The corollary to this is that you get a savings entry, being the difference between your income and your spending. This number gives you a healthy little panic attack when it goes negative, meaning that you broke the cardinal rule. See equation 1!

- Don't accrue more debt while you're paying it off. My general financial awareness improved by several orders of magnitude when I set a personal moratorium on credit card spending. When you're spending real money instead of pretend numbers on a statement, you suddenly care a lot more. A couple of times I've gotten pretty close to being genuinely broke, and then had to become a serious cheapskate for a week or so until my next paycheck came in. It was a good experience. While I was previously in a pretty good habit of paying off what I spent on the credit card (above a certain amount of permanent balance; bad me!), it just feels different when you feel each purchase rather than just tossing whatever lump sum you've got around on the card later. I'm definitely spending less on trivial things this way.

Some Final Thoughts

Tracking my spending and building a real budget has been quite an illuminating process, and is actually kind of fun. You don't need to learn complicated software or get a budgeting app, and the manual process is probably more satisfying anyway. Give it a try!

resolutions

resolute, adj.: Admirably purposeful, determined, and unwavering.

resolution, n.: A firm decision to do or not to do something.

Like everyone else on the planet, I've been thinking about this whole 'resolution' concept that goes along with buying a new calendar and remembering to increment the year when dating things (surely I'm not the only one who will keep accidentally writing 2011 until at least February, yes?). The most traditional resolutions are things like getting in shape, eating better, spending less, losing weight, and being a better person. While these things are certainly admirable and are helpful long-term notions, the thought of measuring one's ability to 'achieve' such vague goals come the next calendar-buying-season is less than appealing. Besides, that sort of thing belongs on my 'long-term goals' page, not in a format that is intended to be achieved in only a year.

I really like the method that Erin over at unclutterer.com has used in the past, wherein she makes a new goal at the beginning of each month. Rather than long-term lofty goals, these are achievable things, and the format allows focusing on only one thing at a time. I would like to give this a try, and so this is officially my first resolution post.

My personal rules:

- Each goal musts be measurable and definite.

- This blog gets to know how each one goes.

- Each goal should improve my finances, household organization, happiness, sanity, effectiveness, or health.

- Failing is not the end of the world. Progress is good.

I've been remarkably lax in updating this medium, and so for January my goal is to write at least two blog posts on any topics every week. Counting this one, that means I will have at least eight new posts for the month of January. Here goes!